One Of The Best Tips About Modified Opinion Audit Report

10+ Sample Audit Report Templates

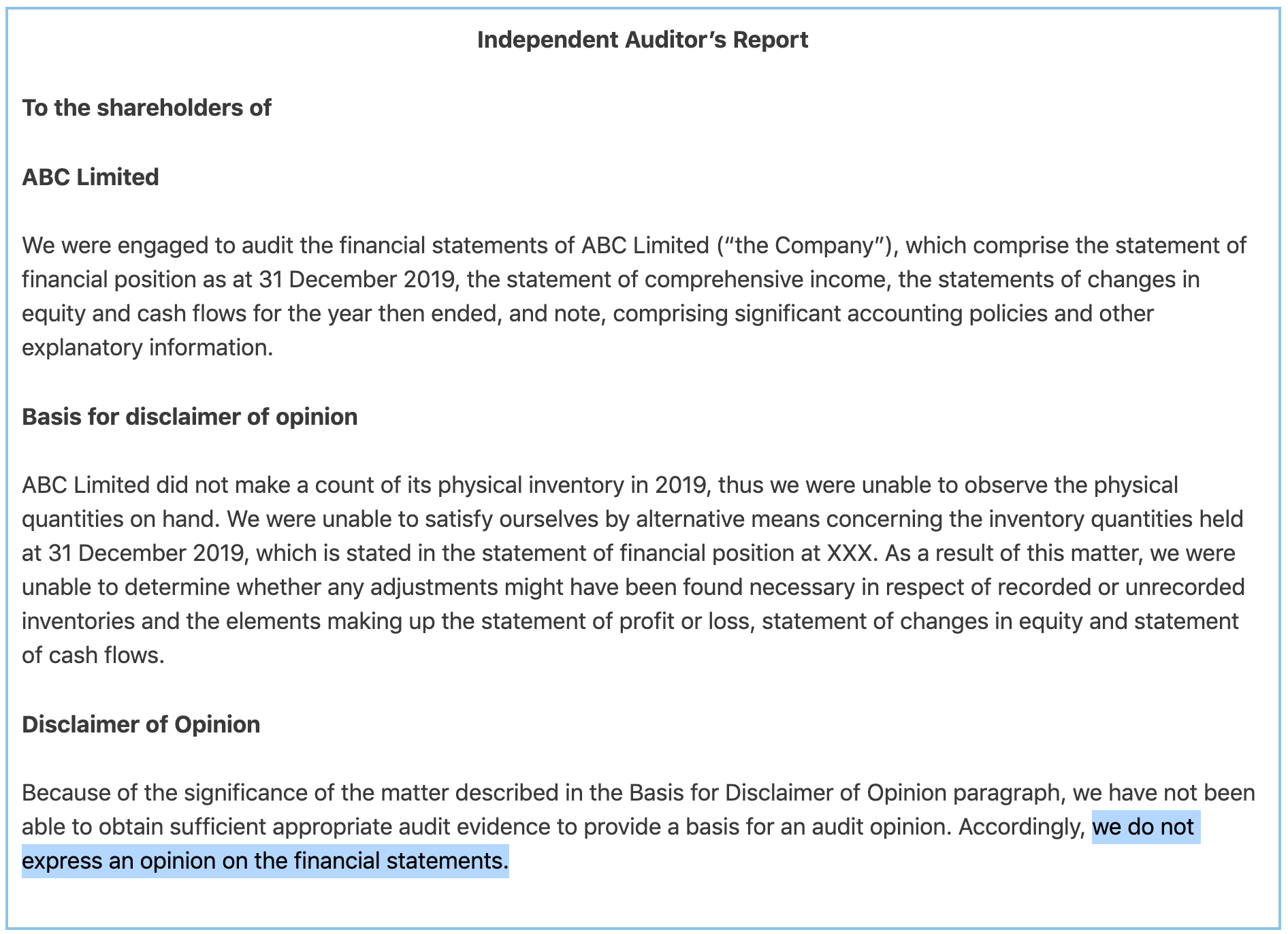

Fabulous Modified Audit Opinion Example Adverse Report Company

Qualified Opinion Definition Example Vs Adverse Accountinguide

(pdf) Do Modified Audit Opinions Have Economic Consequences? Empirical

Ppt Audit Report Powerpoint Presentation, Free Download Id3147284

Modifications to the opinion in the independent auditor’s report 1 singapore standard on auditing ssa 705 (revised) modifications to the opinion in the independent auditor’s report ssa 705 was issued in january 2010.

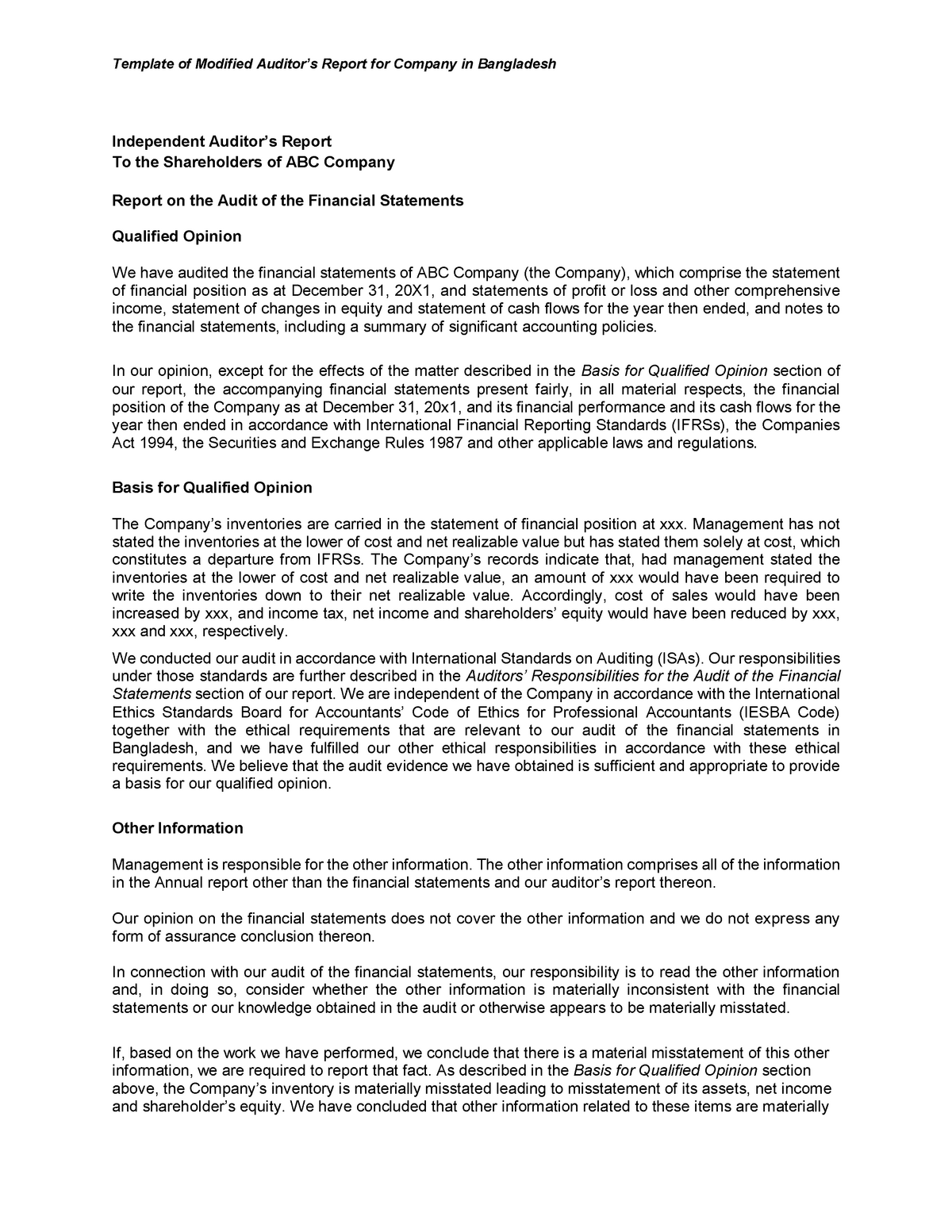

Modified opinion audit report. Additional disclosures in the auditor’s report which are not modifications of the opinion. That is what the auditor's report will say, if there's simply not enough. Auditor’s report for audits conducted in accordance with the standards of the pcaob and gaas when the audit is not within the jurisdiction of the

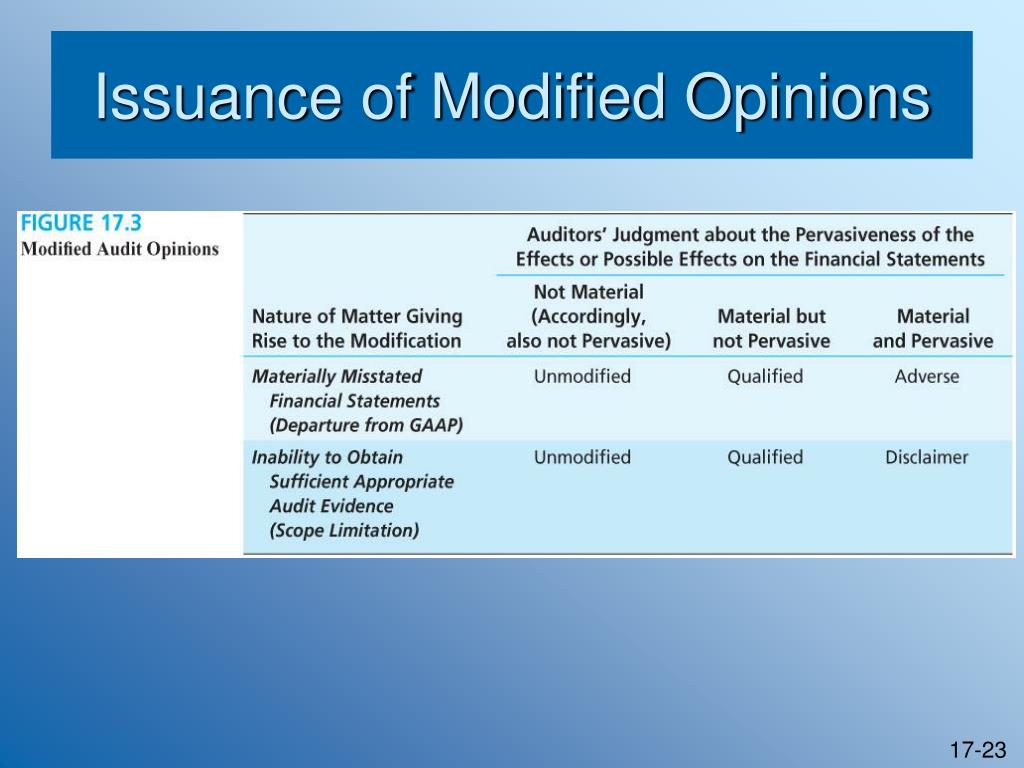

Modified opinions if the audit report is not “clean” or “unmodified” then the modification can be one of three main types: The auditor shall express an unmodified opinion when the auditor concludes that the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. Technical helpsheet issued to help icaew members to identify the various changes that may need to be made to audit reports under international standards of auditing (uk) where there is a modified opinion,.

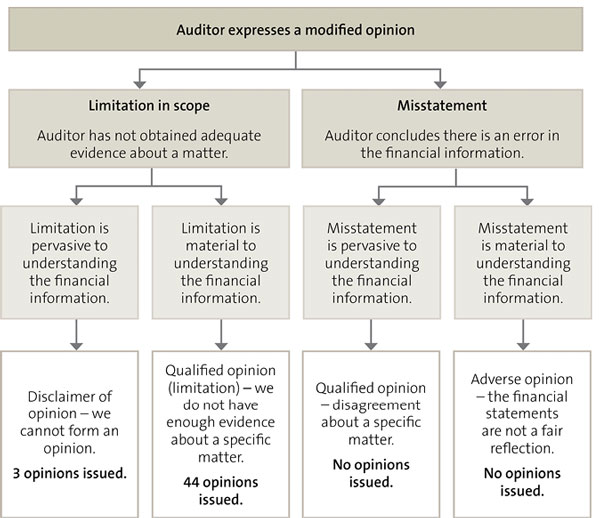

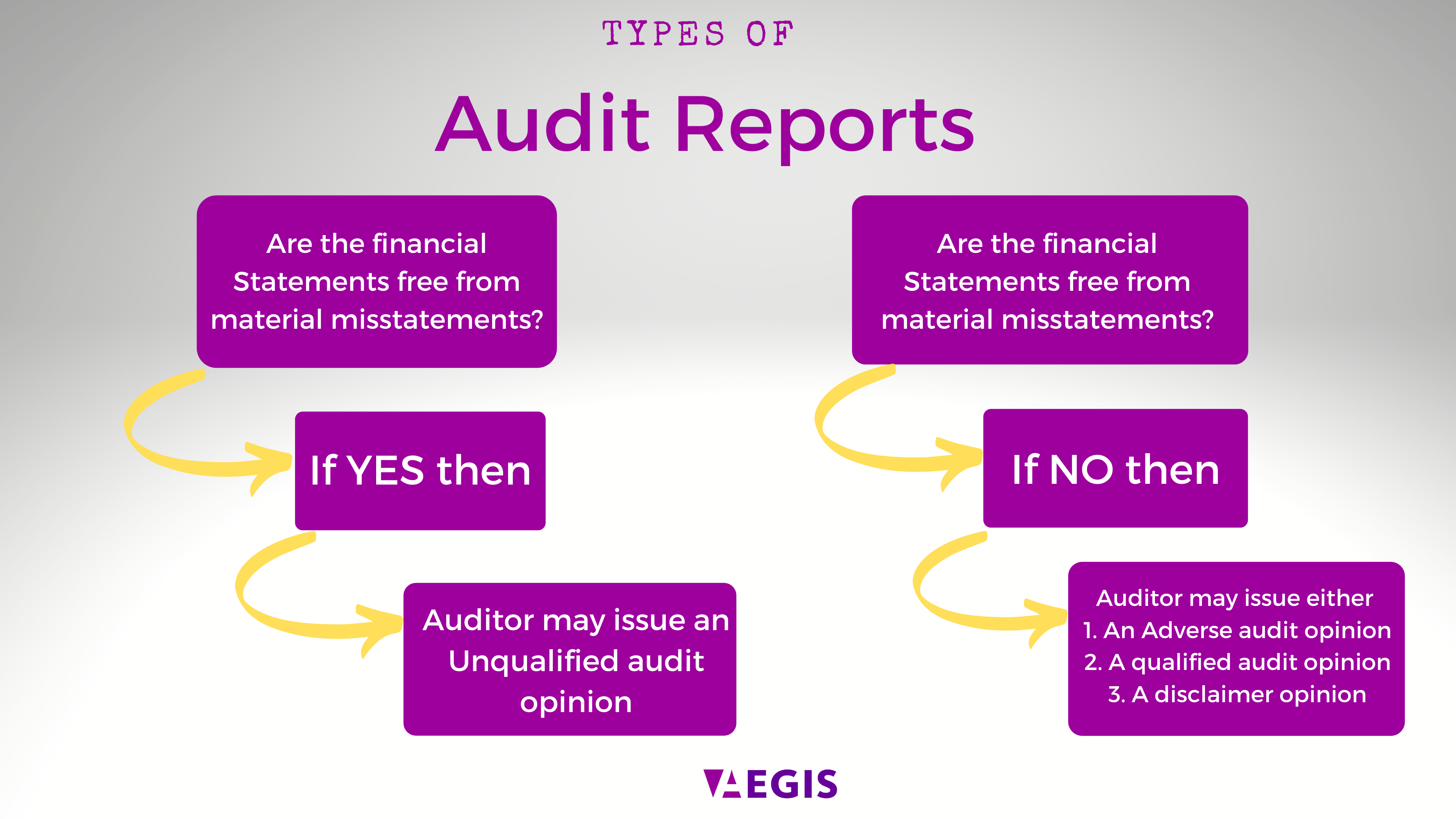

This standard on auditing (sa) deals with the auditor’s responsibility to issue an appropriate report in circumstances when, in forming an opinion in accordance with sa 700 (revised),1 the auditor concludes that a modification to the auditor’s opinion on the financial statements is necessary. Audit opinion flow chart. The companies (amendment) act 2014 gave rise to conforming amendments in ssa 705 in june 2015.

Modifications to the opinion in the independent auditor’s report1233. 1 modified audit opinions 1.1 reasons for modifying the opinion 1.2 materiality and pervasiveness 1.3 wording a modified opinion 1.3.1 illustration of a qualified opinion 1.3.2 illustration of a qualified opinion 1.3.3 illustration of an adverse opinion 1.3.4 illustration of a disclaimer of opinion modified audit opinions Modifications to the opinion in the independent auditor's report hong kong standard on auditing 705 (revised) effective for audits of financial statements for periods ending on or after 15 december 2016 hksa 705 (revised) issued august 2015;

The other type of audit opinion is modified opinion, classified into three categories as explained below. The international auditing and assurance standards board (iaasb) finalised its project on auditor reporting in 2015, which resulted in a set of new and revised standards on auditor reporting as well as revised versions of isa, 570 going concern and a number of other international standards on auditing (isas). Modifications to the opinion in the independent auditor's report hong kong standard on auditing 705 (revised) effective for audits of financial statements for periods ending on or after 15 december 2016 hksa 705 (revised) issued august 2015;

The complete form and content of the unmodified opinion are presented in isa 700, forming an opinion and reporting on financial statements. (i) qualified (ii) adverse (iii) disclaimer. A modified opinion can also take the form of no opinion at all, which is called a disclaimer of opinion.

Modifications to the opinion in the independent auditor’s report international standard on auditing 705 (revised) modifications to the opinion in the independent auditor’s report the malaysian institute of accountants has approved this standard in july 2022 for publication. Types of modified opinion the decision as to which type of modified opinion is appropriate depends upon: Instructions when a compliance audit is combined with a financial audit, the opinion on the aspect of compliance should be clearly separated from the opinion on the financial statements.

The basics when an auditor is able to satisfactorily conclude that the financial statements are free from material misstatement they express an unmodified opinion. These are types of opinions that the auditor issues to the company if its financial reporting is done per the entity’s accounting standards. An unmodified opinion, auditors issue this opinion to financial statements prepared in all material respect and comply with accounting standards being used and the applicable regulation.

Revised january 2016, august 2016, june 2017 In general, there are two main types of audit opinions: Revised january 2016, august 2016, june 2017, december 2021, march 2023

Modified Opinion Audit Report Example Financial Statement Alayneabrahams

Modified Audit Opinions Determining Which Is Appropriate Cpa Hall Talk

Ppt Sa 700 (revised), 705 & 706 Powerpoint Presentation, Free

Audit Report Qualified Opinion Impact Of

Ppt New Audit Reporting Standards Powerpoint Presentation, Free

Audit Opinion Examples Dewsp

Audit Assignment 4 Types Of Opinions

Modified Audit Reports Past Questions Youtube

Modified Audit Opinion

Ppt New Audit Reporting Standards Powerpoint Presentation Id1555836

Audit Opinion Types Available In Our Europe Database

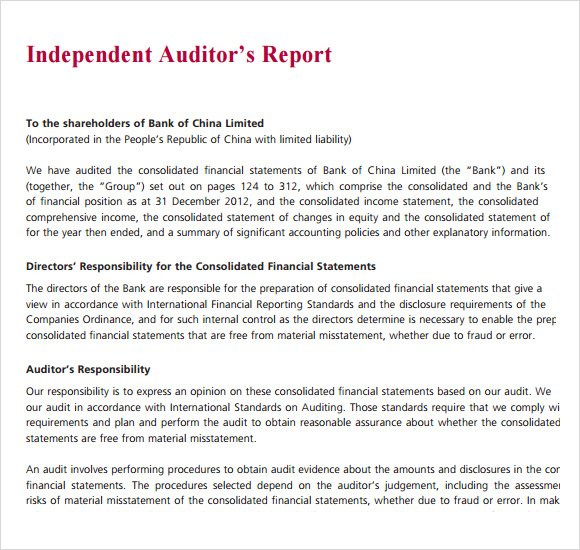

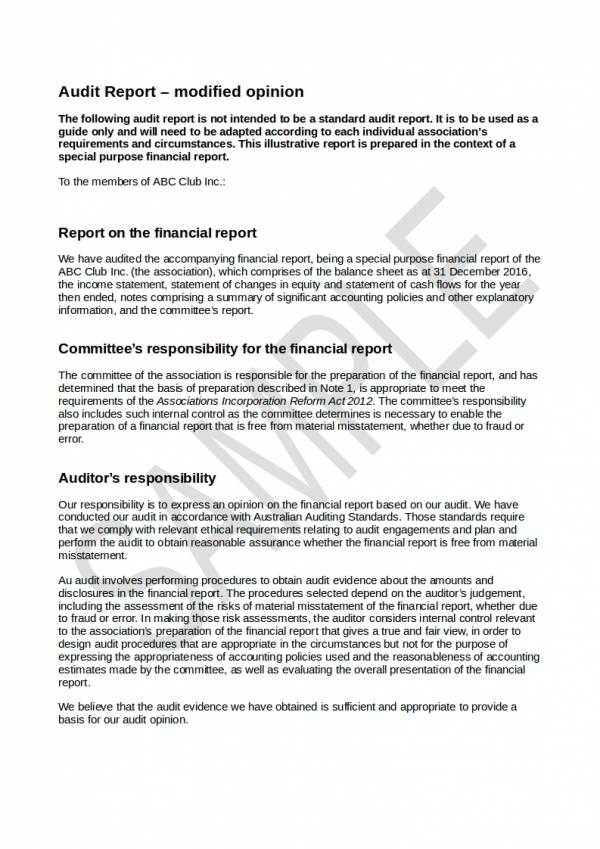

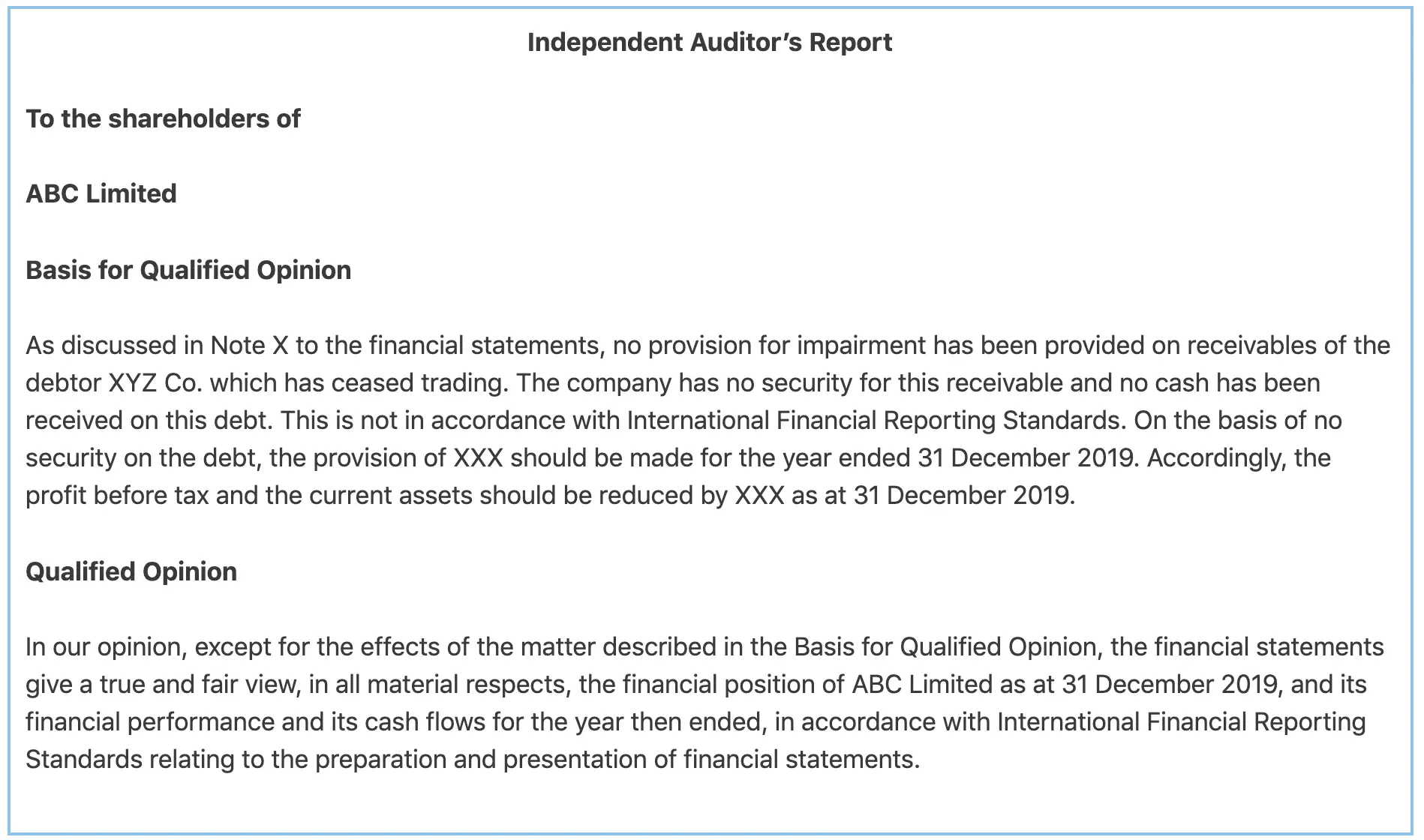

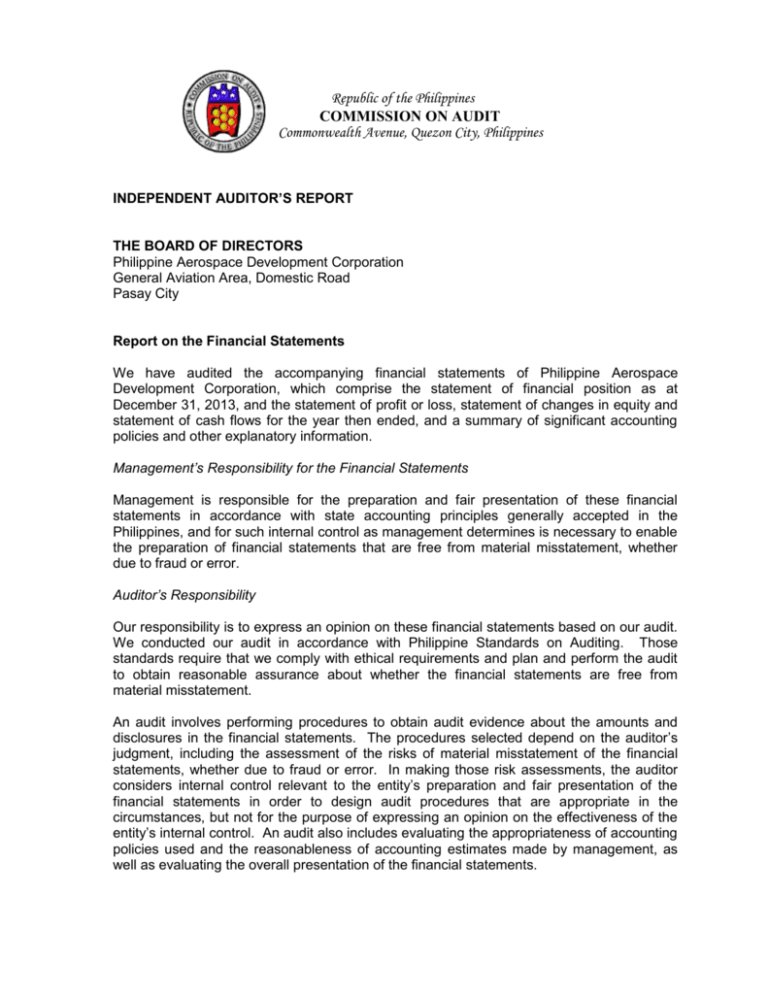

Independent Auditor's Report Philippine Aerospace Development With