Glory Tips About Direct Indirect Cash Flow Statement

Cash Flow Statement Indirect Method Vs Direct

Cash Flow Statement Direct And Indirect Method My Xxx Hot Girl

Cash Flow Statement Indirect Method Vs Direct

The Ultimate Guide To Indirect Cash Flow 2023 Atonce

Direct Cash Flow Vs. Indirect

What’s The Difference Between Direct And Indirect Cash Flow Methods

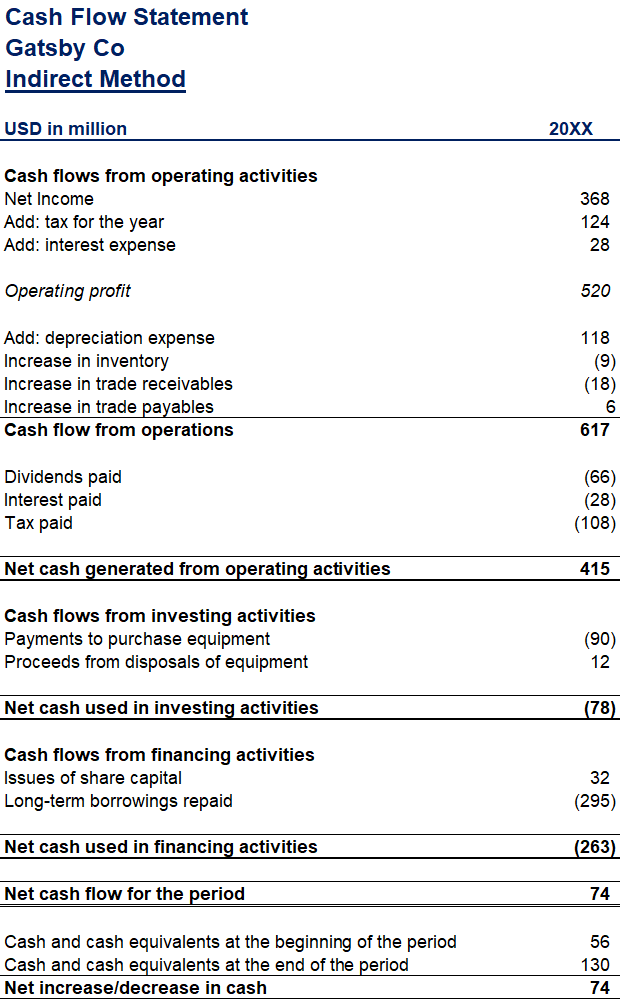

Cash flow statement (cfs) is a financial statement that reconciles net income based on the actual cash inflows and outflows in a period.

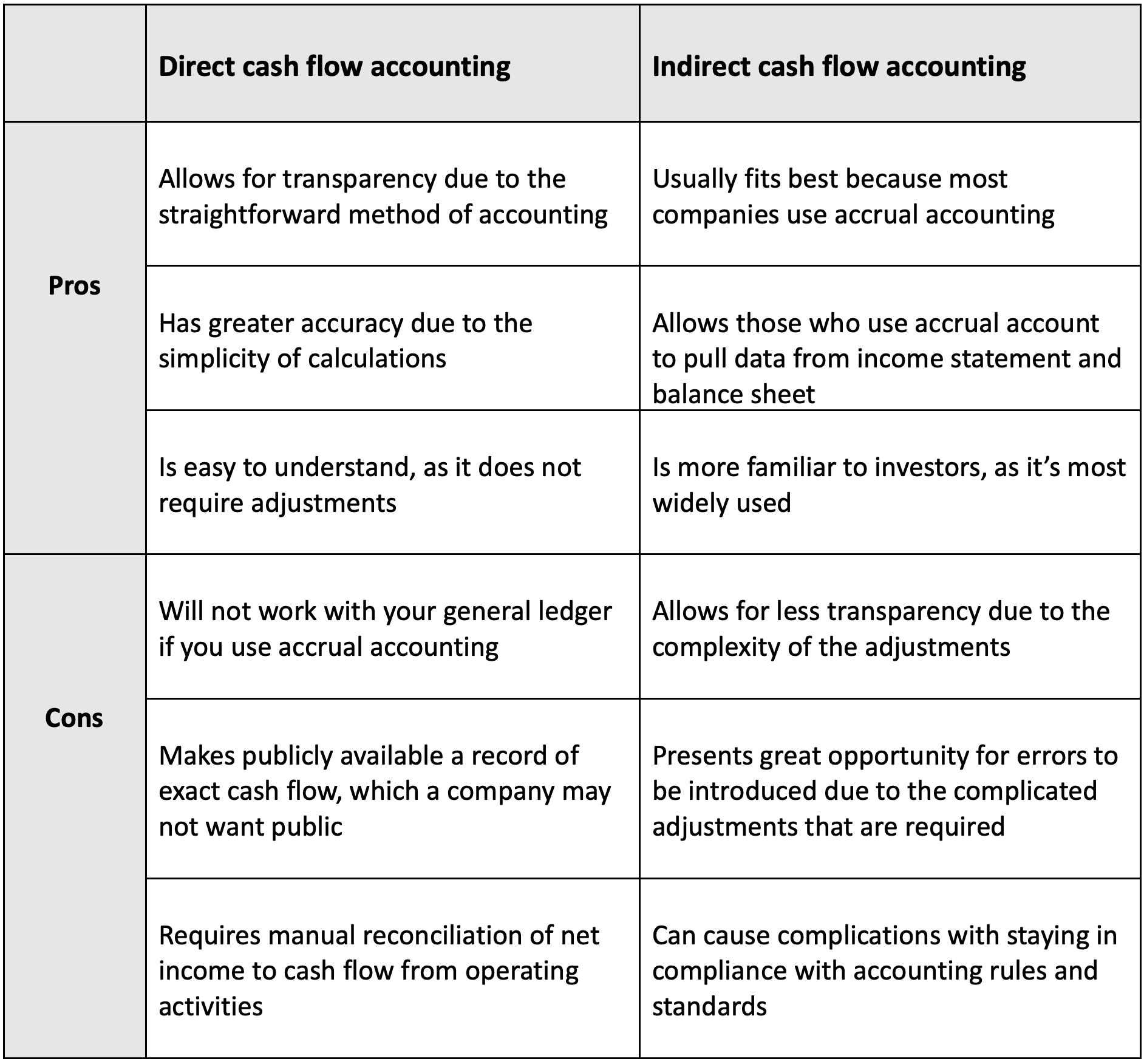

Direct indirect cash flow statement. As we discussed above, the direct method offers great granularity and detail about what activities are contributing to the business’s net cash flows. Cash flows are classified and presented into operating activities (either using the 'direct' or 'indirect' method), investing activities or financing activities, with the latter two categories generally. The two methods by which cash flow statements (cfs) can be presented are the indirect method and direct method.

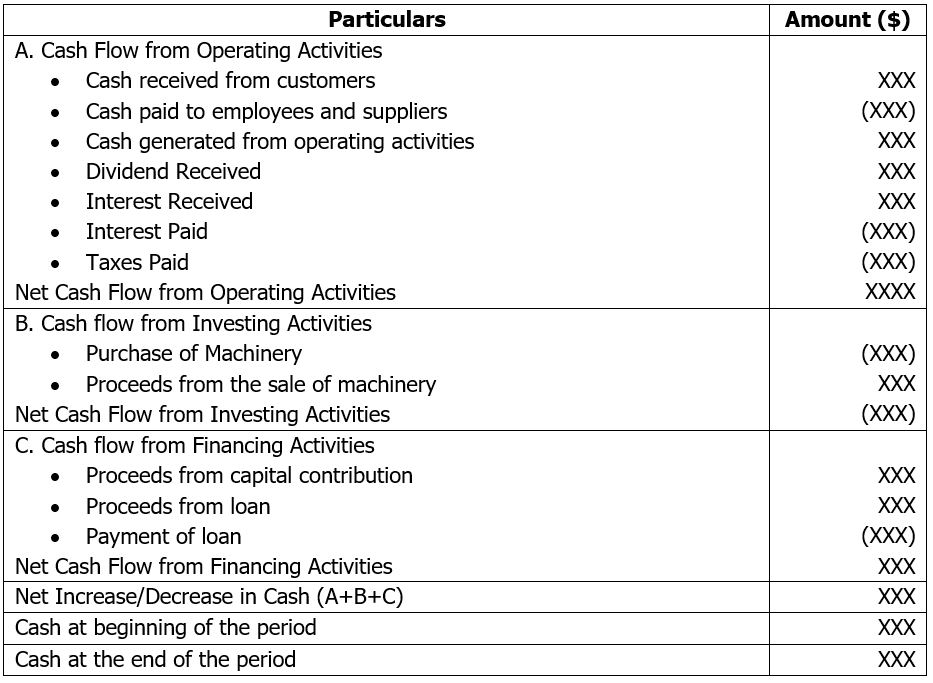

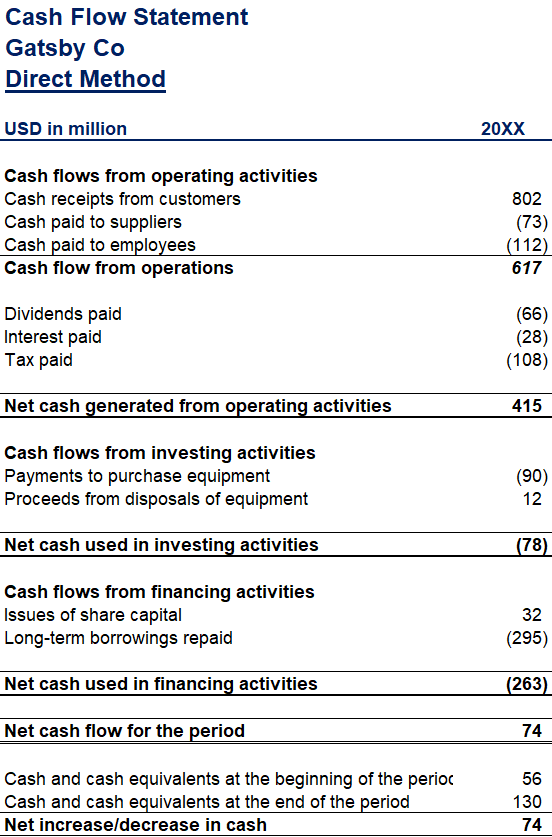

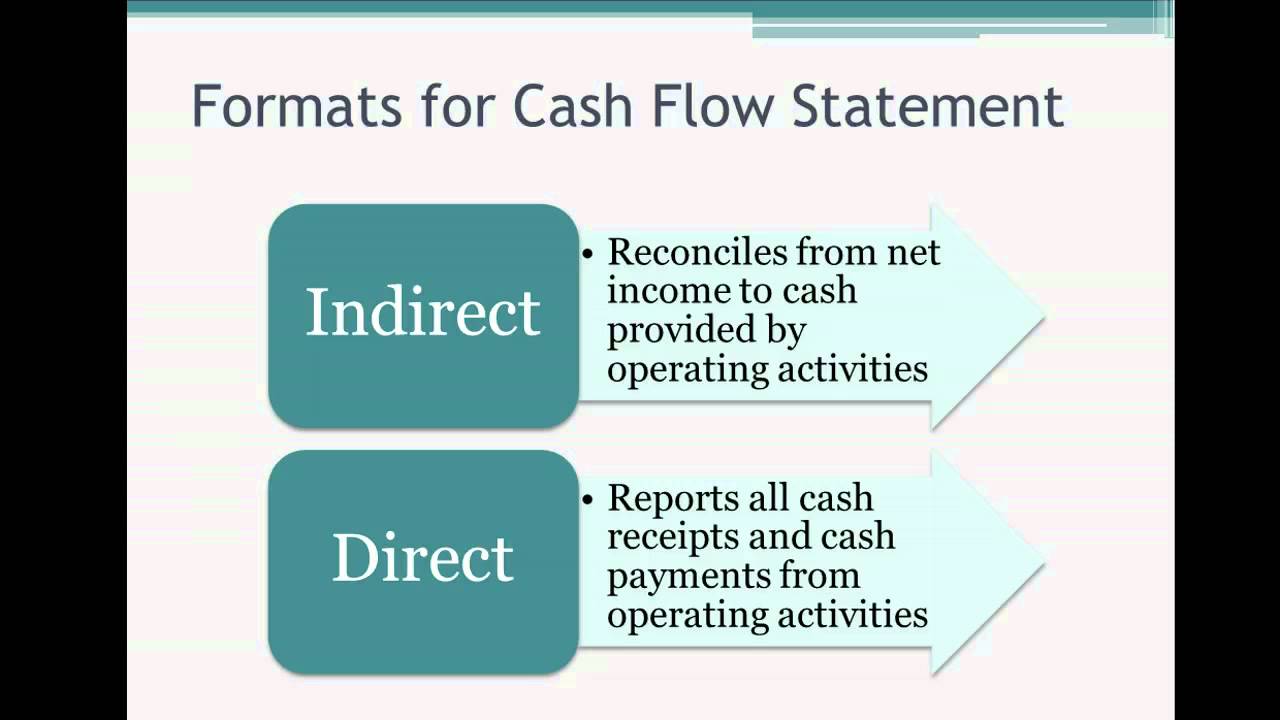

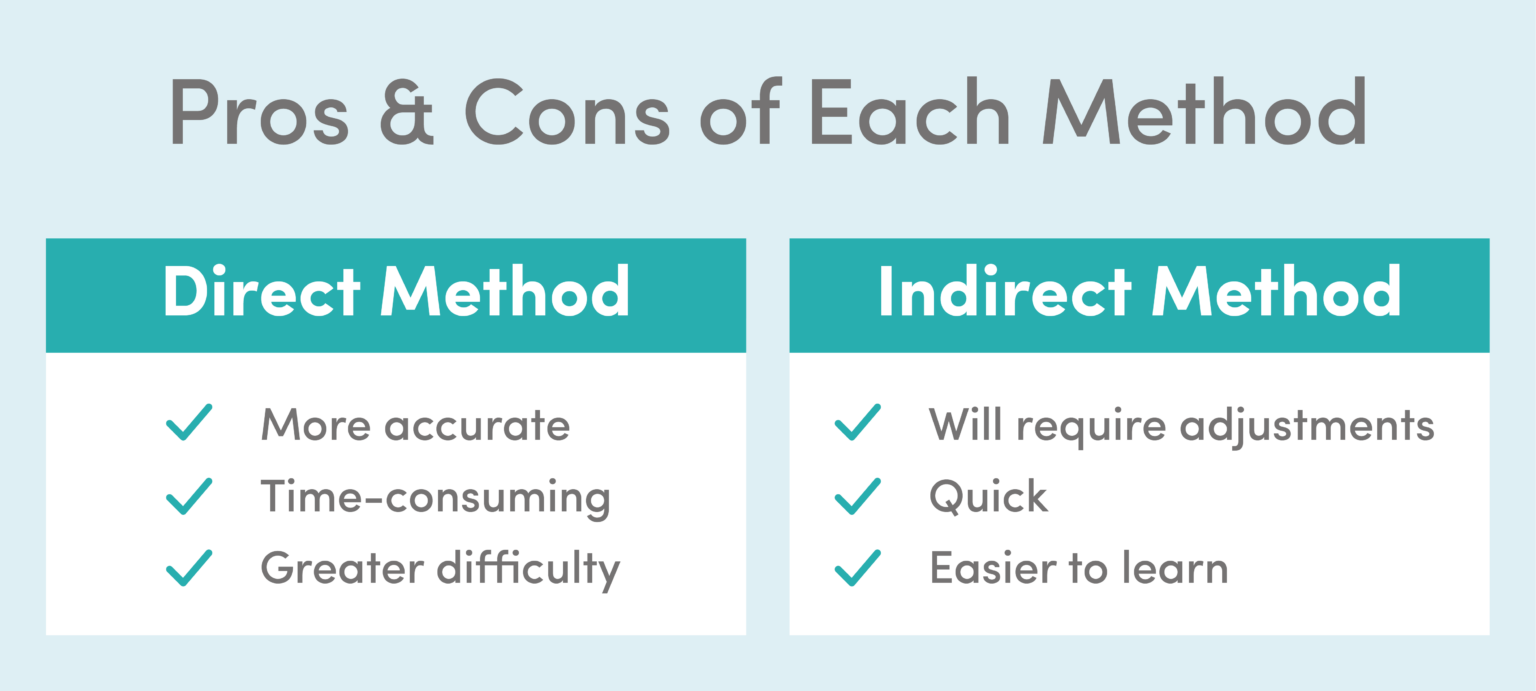

The indirect method will require additional adjustments to the cash flow statement. Direct method the cash flow statement is divided into three categories— cash flows from operating activities, cash flows from investing activities, and cash. The cash flow from the operations section of the cash flow statement can be prepared using either the direct method or the indirect method.

Although the fasb favors the direct method, accountants tend to prefer the indirect method because it can be accomplished much quicker than its counterpart. A company’s cash flow statement can be prepared with either the direct or indirect cash flow accounting method. Factoring in the direct and.

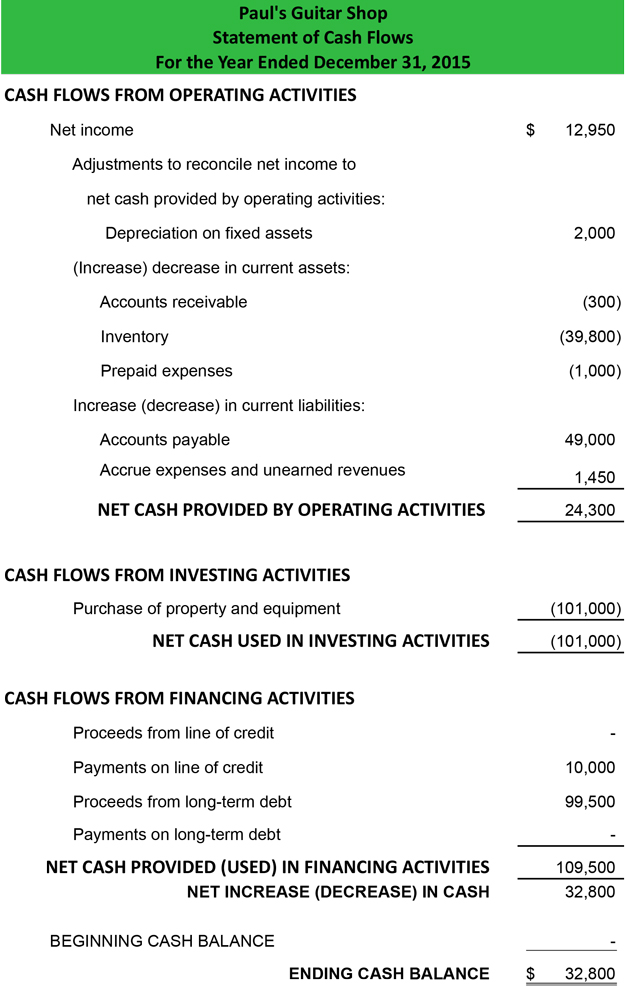

The statement of cash flows prepared using the indirect method adjusts net income for the changes in balance sheet accounts to calculate the cash from operating activities. In the direct method of cash flow statement preparation, actual receipts from customers and actual payments to suppliers, service providers, employees, taxes, etc. For example, if a retailer sells an item on credit, the indirect method.

As the company is hit by regulatory action by the reserve bank of india, the brokerage decided not to rate the stock, it said in a feb. Only the operating cash flow section of the cash flow statement can be prepared using the direct or the indirect method. Indirect cash flow method is the type of transactions used to produce a cash flow statement.

The advantage of the direct method over the indirect method is that it reveals operating cash receipts and payments. The two methods of calculating cash flow are the direct method and the indirect method. Indirect method vs.

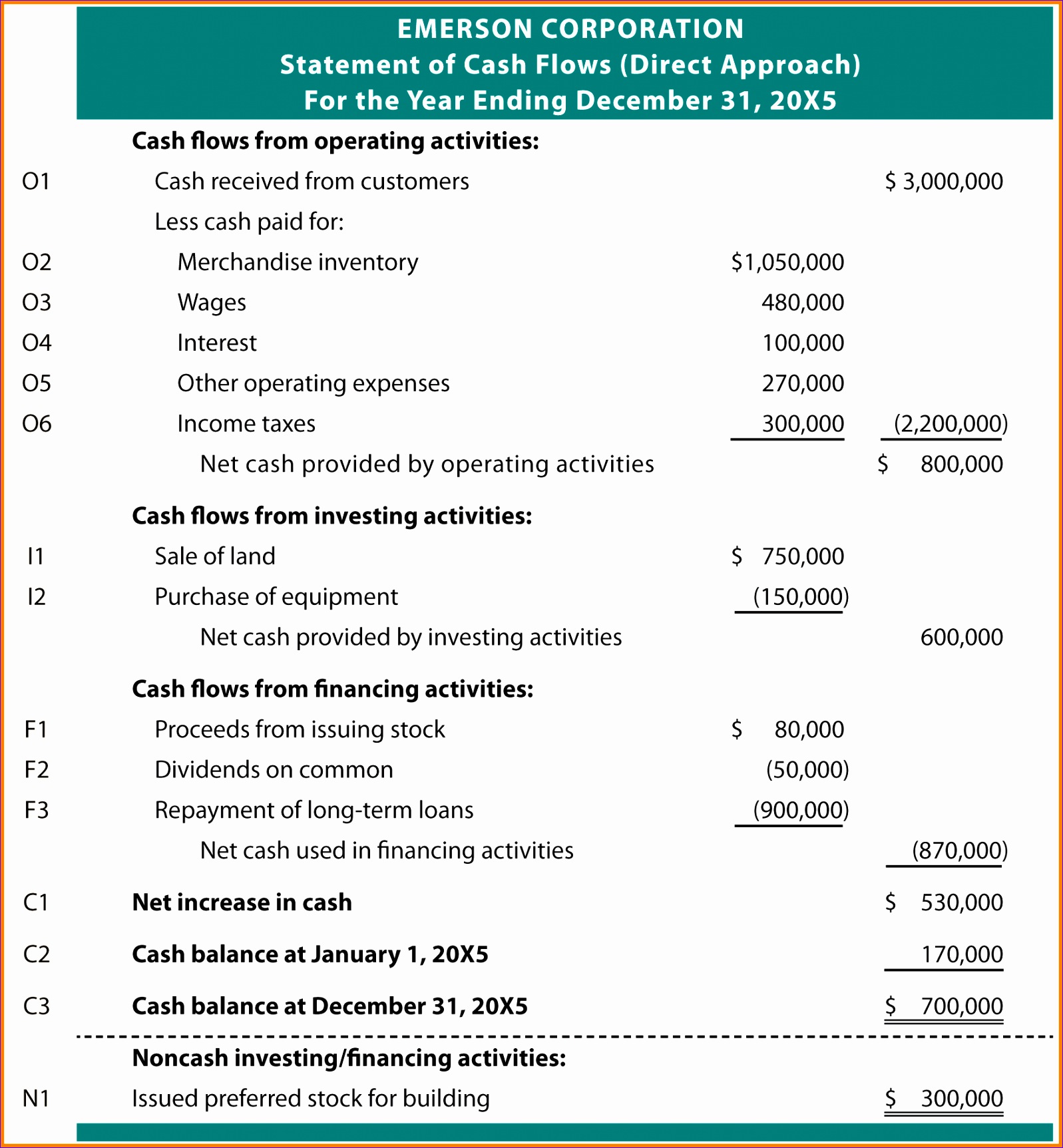

For instance, assume that sales are stated at $100,000 on an accrual basis. Ias 7 statement of cash flows requires an entity to present a statement of cash flows as an integral part of its primary financial statements. The direct method and indirect method of preparation of cash flow statement differ in the way the cash flows from operating activities is calculated and presented.

You can gather this information from the company’s balance sheet and income statement. The indirect method focuses on net income and may include cash that is not yet in the business. In this article, we explore direct and indirect cash flow, highlight their most notable differences and provide an example of a cash flow statement using both methods.

Direct and indirect cash flow statements. The direct method converts each item on the income statement to a cash basis. The indirect method for the preparation of the statement of cash flows involves the adjustment of net income with changes in balance sheet accounts to arrive at the amount of.

Begin with net income from the income statement. The direct method, and the indirect method. Blog overview in this article we are going to address the following:

Bok Drury

Example Of A Statement Cash Flows Direct Method, Forex Trading

Cash Flow Statement Indirect Method Vs Direct

12.1 Cash Flow Statement Direct Vs Indirect Method Youtube

Direct Vs Indirect Cash Flow Methods Top 7 Differences (infographics)

Cash Flow Statement Excel Templates

Direct Vs. Indirect Cash Flow

Direct Vs Indirect Methods Of Cash Flow Accounting Versapay

Direct Vs Indirect Cash Flow Gaap Blimp Microblog Custom Image Library

Statement Of Cash Flows Indirect Method Format Example Preparation

What’s The Difference Between Direct And Indirect Cash Flow Methods

What’s The Difference Between Direct And Indirect Cash Flow Methods

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example