Neat Tips About Notes Payable Cash Flow

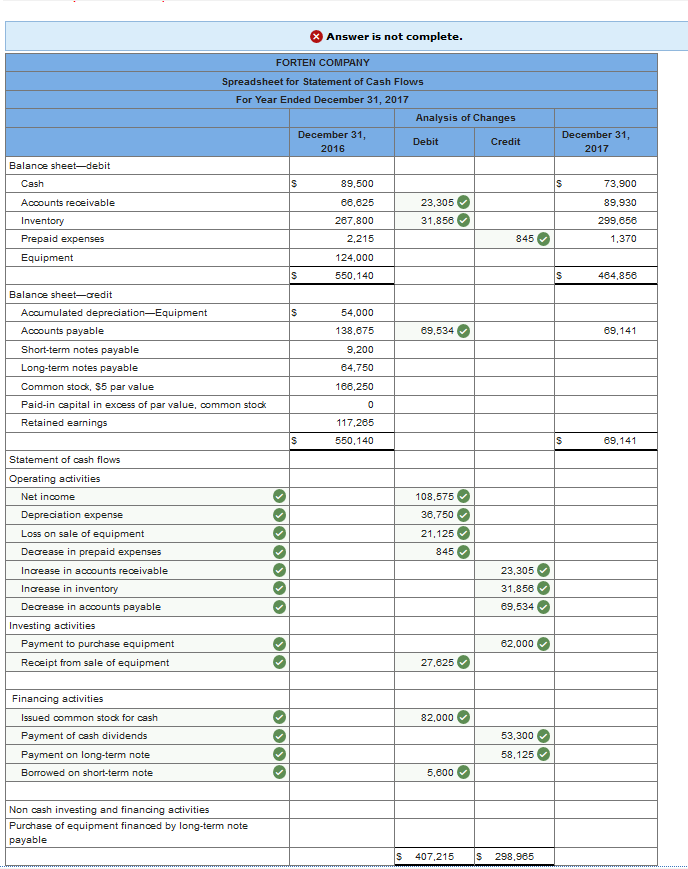

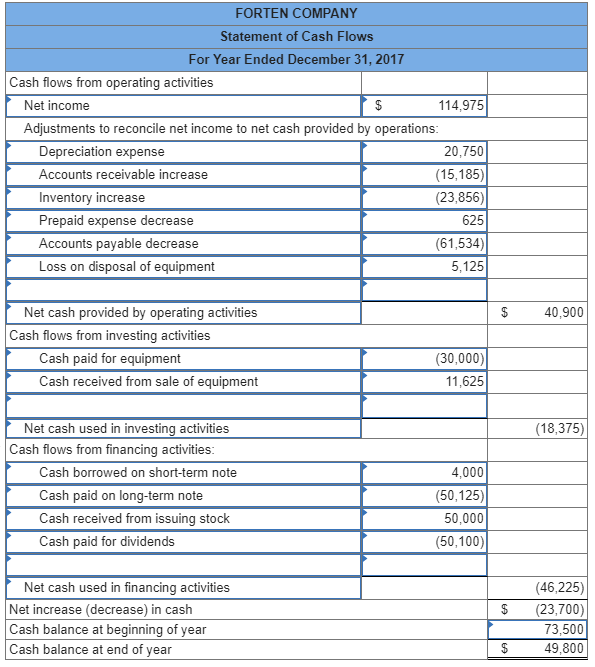

Solved Forten Company, A Merchandiser, Recently Completed

:max_bytes(150000):strip_icc()/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

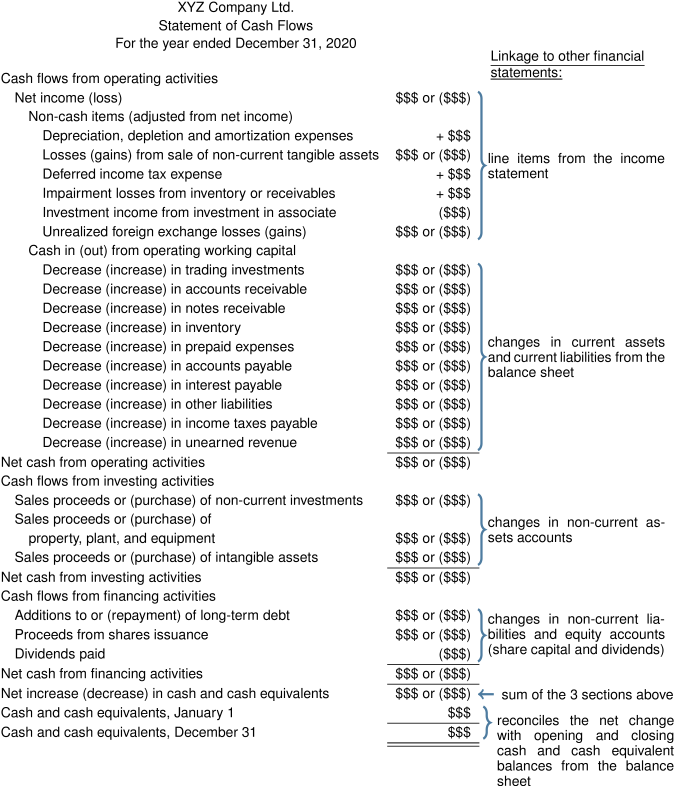

Cash Flow Statement What It Is + Examples

Casual Adjusting Entry For Notes Payable Cash Flow Indirect Method Template

Think Profit! Part 3 Cash Flow Furniture World Magazine

Cash Flow Spreadsheet Template Free Downloa

Mbatabfinancial Accounting Blog Cash Flow Statement Analysis

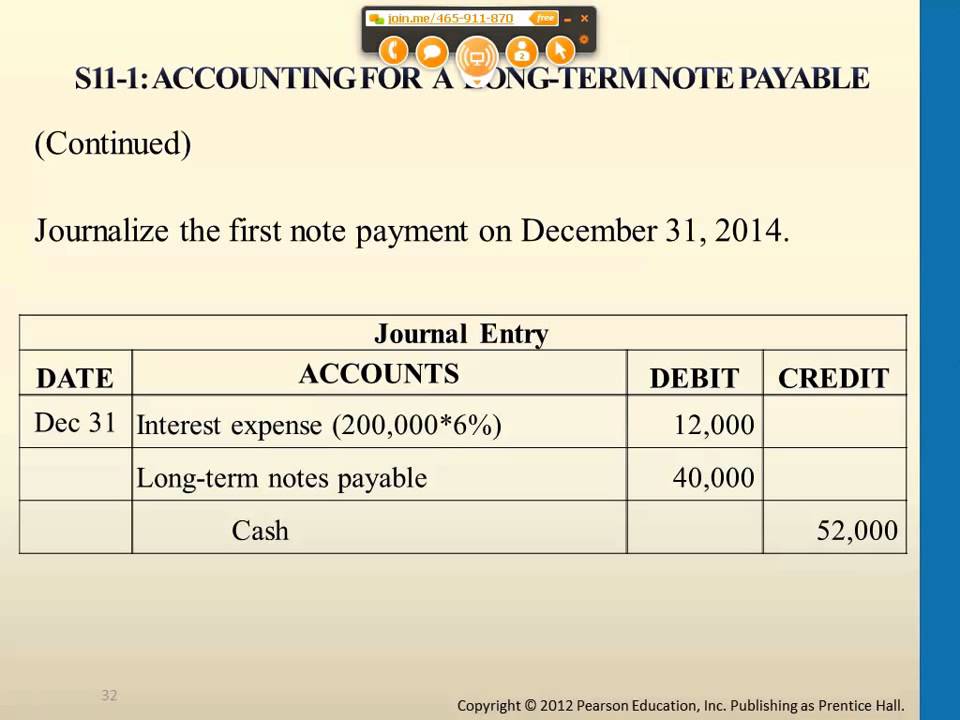

The maker then records the loan as a note payable on the balance sheet.

Notes payable cash flow. Most companies are required to produce this. If a company borrows capital under a note. Cash flow statements (cfs) provide a summary of the cash that a company brings in and spends in a given time period, also called cash inflow and cash outflow.

However, they differ in payment terms and whether they involve regular interest payments. It is supported by a formal. A note payable affects the cash flow statement by reducing the amount of cash that a company has available, as payments must be made to repay the loan.

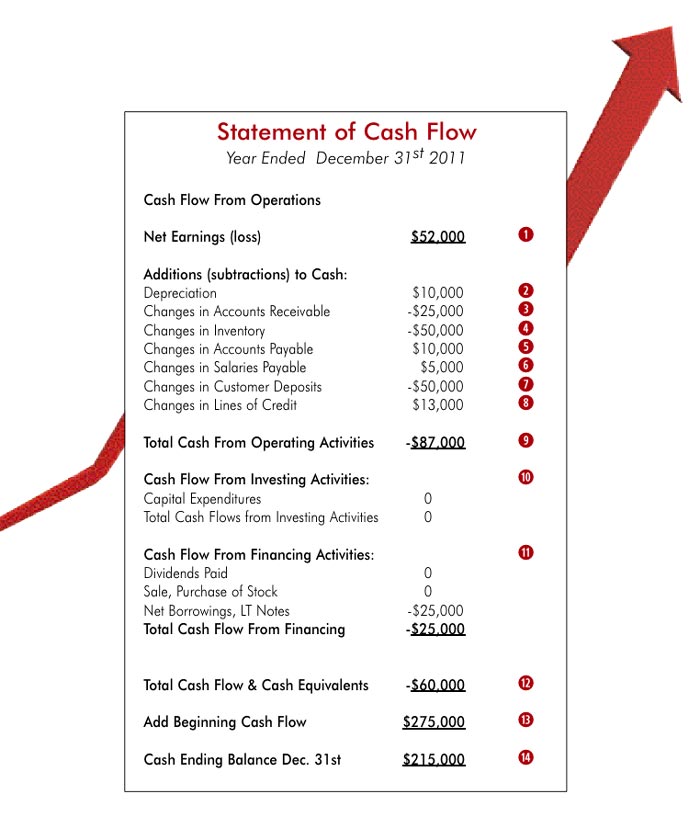

To provide clear information about what areas of the business generated and used cash, the statement of cash flows is broken down into three key categories: The interest paid on a note payable is reported in the section of the cash flow statement entitled cash flows from operating activities. Notes payable have an effect on cash flow when a company receives or pays back the proceeds and when it makes regular interest payments.

Recording a notes payable includes specifying details and terms of the agreement,. While accounts payable often involve. Since most corporations report the cash.

Notes payable are the corresponding liabilities on a maker’s books, also in the amount of outstanding principal. Interest expense increases (a debit) for $4,500 (calculated as $150,000. The notes payable account in the liabilities section of the balance sheet represents the total.

Both types of payables appear as liabilities on the balance sheet; For the entity doing the lending, also known as a. A note payable is an unconditional written promise to pay a specific sum of money to the creditor, on demand or on a defined future date.

A note payable is a debt that is established with a written agreement. Capital borrowing journal entry (debit, credit) cash account: Managing these two liabilities is crucial for businesses to maintain healthy cash flows and ensure timely payments to vendors and lenders.

Common examples of current liabilities include accounts payable, unearned revenue, the current portion of a noncurrent note payable, and taxes payable. 11.3 accounts and notes payable publication date:

20.2 Statement Of Cash Flows Indirect Method Review Intermediate

Steps To Prepare Statement Of Cash Flows Finance Train

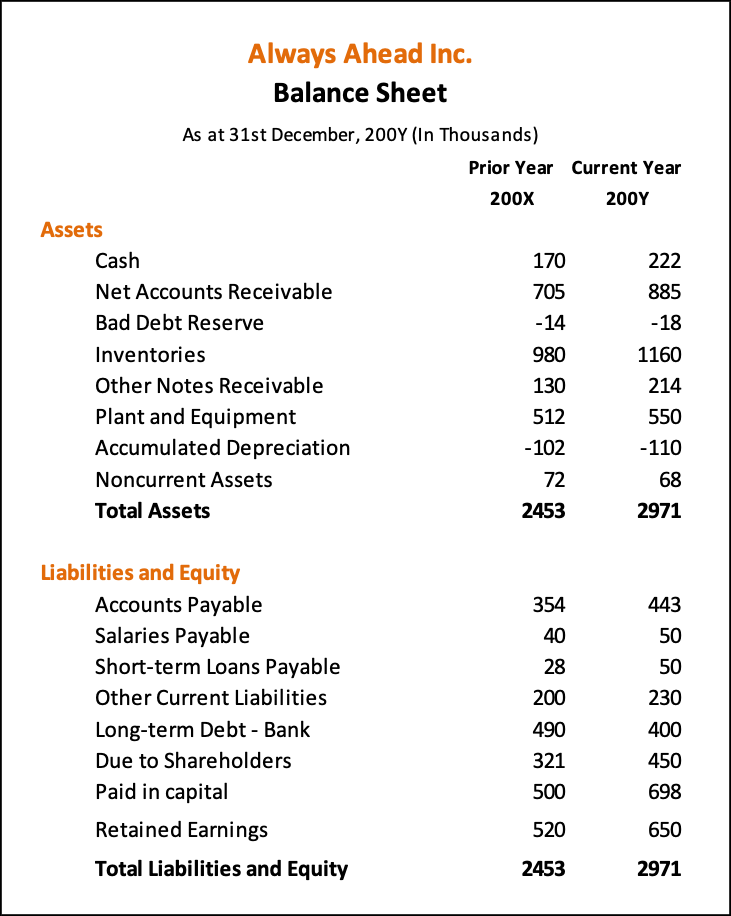

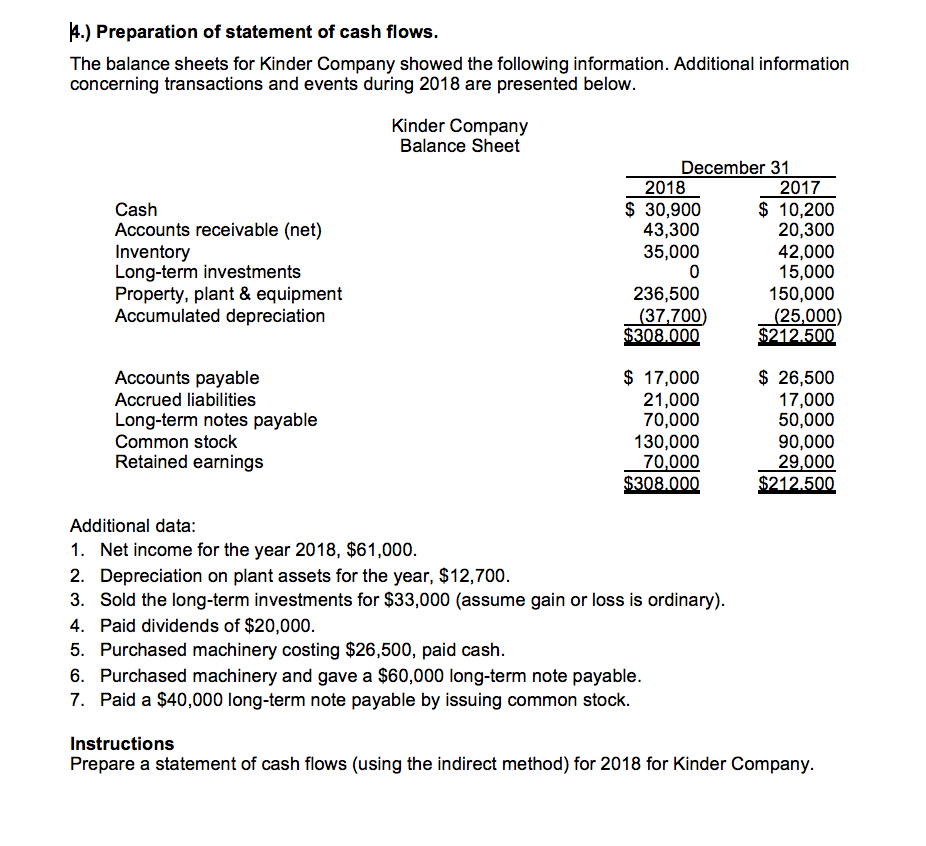

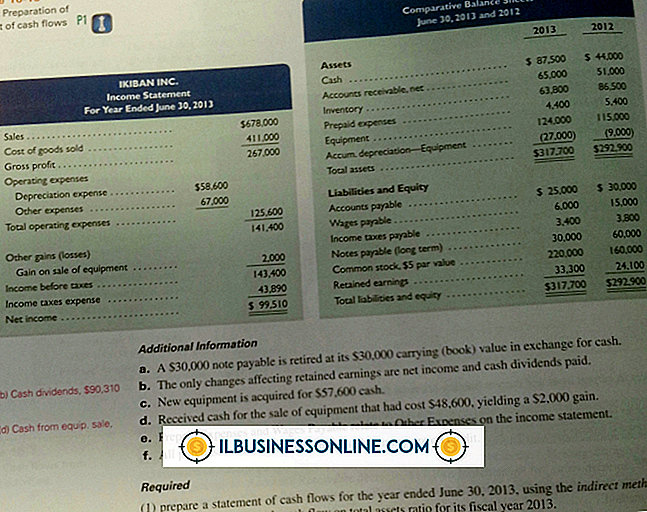

Solved 4.) Preparation Of Statement Cash Flows. The

Quiz And Homework Chapter 12 Indirect Statement Of Cash Flows

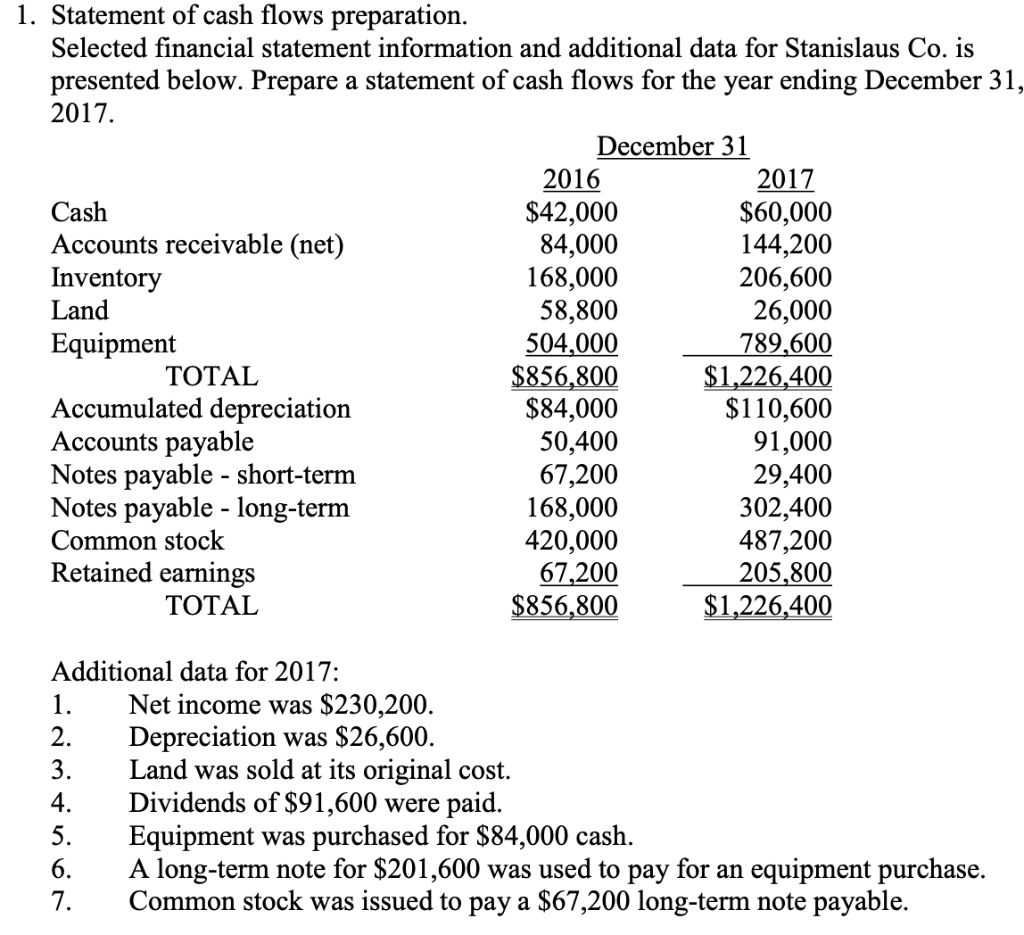

Solved 1. Statement Of Cash Flows Preparation. Selected

Cash Flow Statement Finance Train

What Is Reported On The Statement Of Cash Flow?

The Cash Flow Statement And It’s Role In Accounting

Statement Of Cash Flow Template Direct Method Addictionary

How To Draw Up A Cash Flow Statement Fitzgerald Dearthe

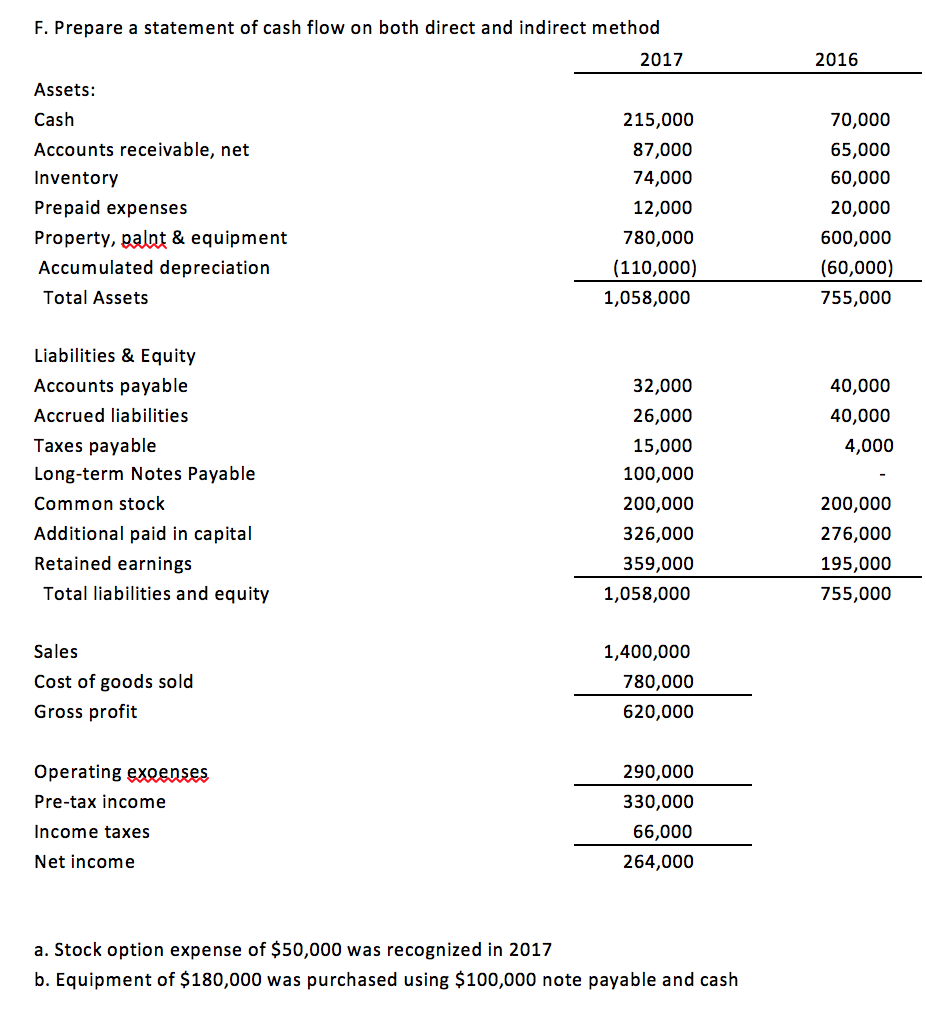

Solved F. Prepare A Statement Of Cash Flow On Both Direct

Kindle Fireでcookieを有嚹にする方法