Divine Tips About Change In Equity From Nonowner Sources Is

What Is Private Equity? Euromoney Learning Ondemand Powered By

How Does Sweat Equity Work? Trica Blog

Equity Handwriting Image

Share Cfd Trading Trade Stock Cfds Fp Markets

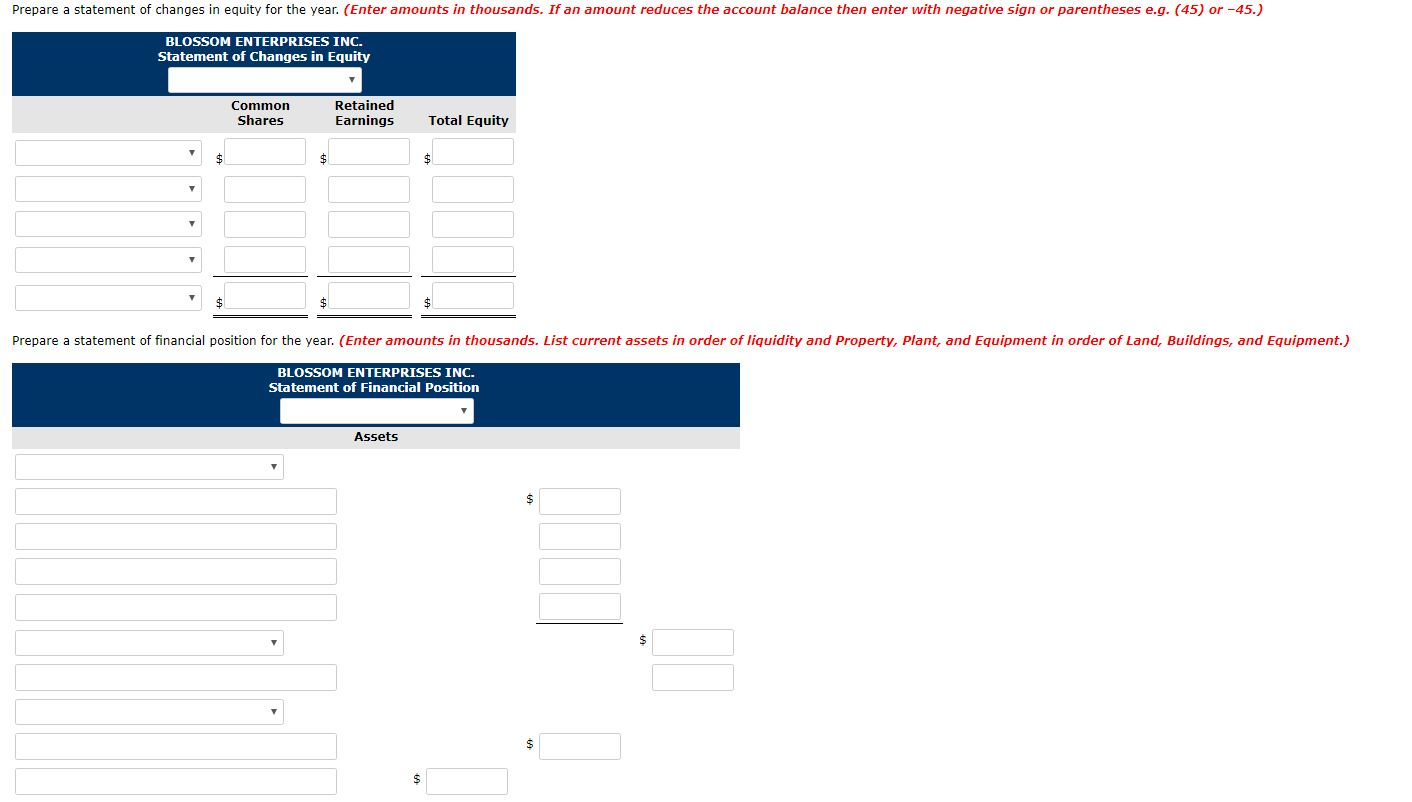

Solved Prepare A Statement Of Changes In Equity For The

"how To Calculate Return On Equity Ratio Like A Pro 5 Simple Steps For

Statement of changes in equity, often referred to as statement of retained earnings in u.s.

Change in equity from nonowner sources is. Equity is a residual amount, the owners’ interest in assets after subtracting liabilities. The change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources. Comprehensive income does not include changes in equity caused by the actions of the owner of the business, such as dividends and the sale or purchase of.

It includes all changes in equity during a period except those resulting from investments by owners and distributions to owners.” comprehensive income is the sum of net income and other items that must bypass the income statement Distribution to owners—cash, other assets, or ownership interest (equity) provided to owners. Change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources corporation legal business structure.

This problem has been solved! Income as “… the change in equity of a business during a period from transactions and other events and circumstances from nonowner sources. Change in equity from nonowner sources include all equity transactions, other than changes resulting from prior transactions with the shareholders of the company.

Accounting accounting questions and answers comprehensive income is the change in equity from: It includes all changes in equity during a period except those resulting from investments. The change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources.

Gaap, details the change in owners’ equity over an accounting period by. There are four categories of items. Change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources current ratio current assets divided.

Comprehensive income —defined as the “change in equity of a business. Change in equity from nonowner sources is: The change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources is called click the card to flip 👆.

It includes all changes in. Comprehensive income is the change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources. It includes all changes in.

An enterprise reports comprehensive income—nonowner changes in equity—to reflect all of the changes in its equity resulting from recognized transactions and other. The change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources is called distributions to owners. For a corporation, equity arises primarily from two sources:

The change in equity (net assets) of a business entity during a period from transactions and other events and circumstances from nonowner sources.

Equity Startups

Listed Below Are Several Terms And Phrases Associated With

Equity For All Students Edpuzzle Edtech Methods

Statement Of Changes In Equity

Private Equity Fundraising Euromoney Learning Ondemand Powered By

Equity

Apply For Equity Distribution

Free Of Charge Creative Commons Equity Image Real Estate 1

Southeast Pttc (hhs Region 4) Focus Area Equity Prevention

Pengertian Equity Crowdfunding Beserta Kelebihan Dan Kekurangannya

Equity

Equity Investment Capabilities Invesco Uk

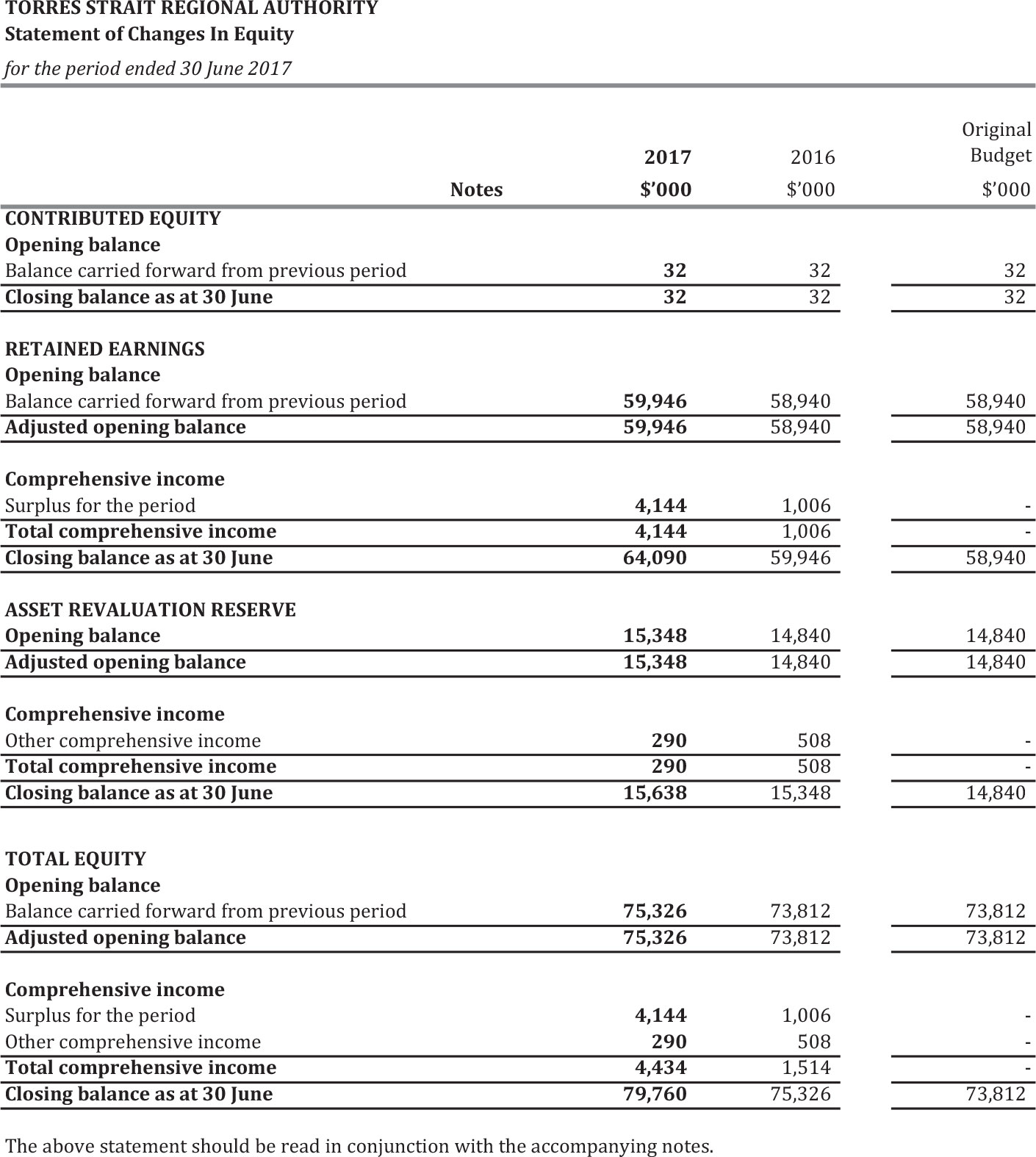

Statement Of Changes In Equity Tsra